In a standard situation, for natural person to be able to deal with financial instruments, natural person opens financial instruments account/securities account or account that is provided by the bank to perform transactions with financial instruments (hereinafter – financial instrument account), and performs transactions with financial instruments (Option 1), or a person can authorize the professional broker to manage its investment portfolio (broker) (Option 2). From 1 January 2018, natural person has an option to open investment account that, in its essence, is financial instruments account that contains a special mark or reference to the status of investment account for the purposes of the Law On Personal Income Tax (PIT Law) (Option 3).

The conditions of PIT application in all three Options are different and accordingly cause impact on the amount of payable PIT and due date of PIT. Transition from one to another option can cause PIT liabilities which in all situations have to be assessed separately. Therefore, before starting to perform transactions with financial instruments, it is recommended to assess PIT liabilities to determine the most appropriate way how to trade with finance assets.

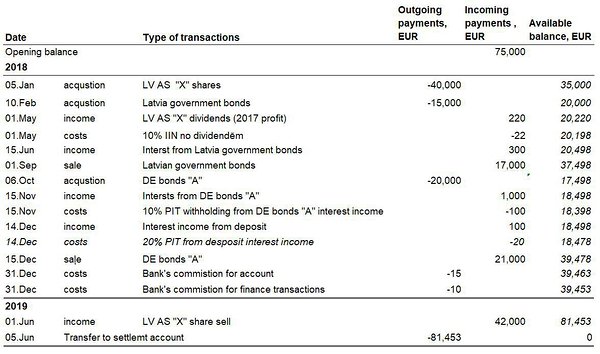

To be able to compare PIT liabilities easily, let’s discuss the following example. Latvian resident, natural person, has performed the following transactions with financial instruments:

Option 1: natural person performs transactions with financial instruments

In Option 1, PIT taxable income is determined by separating:

- income from transactions with capital assets (i.e., income referred to in Section 119 Paragraph 2 of the PIT Law, for example, shares, investment gold, investment funds); and

- income from capital that is not capital gain (i.e., income referred to in Section 119 Paragraph Eleven of the PIT Law, for example, income from bonds, interest and dividends).

Natural person shall declare the income from the capital that is not a capital gain in the annual income declaration to be submitted to the State Revenue Service, in the year following the taxation year, from 1 March to 1 June or from 1 April to 1 July, if income exceeds EUR 55,000.

In the example, in 2018, natural person earned income from capital that is not capital gain (i.e., from bonds, dividends and interest income). Income from Latvia state bonds is non-taxable income, PIT has been withheld from dividends (distribution of profit of 2017) by the income payer, therefore, this received income should not be reported in the annual declaration. Natural person has to declare in annual income declaration for 2018 income from disposal of Bond “A” (i.e., EUR 1,000) and interest income from Bond “A” (i.e., EUR 1,000) from which PIT has been withheld partially, in the amount of 10%.

Thus, in 2018, PIT liabilities of the natural person amounted to EUR 300 (i.e., EUR 21,000 – EUR 20,000+ EUR 1,000) *20% – EUR 100).

In 2019 the natural person earned EUR 2,000 from disposal of shares of AS “X” and natural person is obliged to submit to SRS quarterly declaration until 15 August 2019 for income from capital increase and from income EUR 2,000, 20% PIT, i.e., EUR 400, has to be paid.

Therefore, in this example, in case of Option 1, total PIT liabilities of natural person will amount to EUR 700.

From the administrative point of view, accounting of income and procedure of declaration in Option 1 is complicated and time-consuming, especially for natural persons who are actively performing transactions with financial instruments, as well as in Option 1 it is not possible to use losses of taxation year in following years. Therefore, an active trader, from the point of view of PIT, would not be recommended to use this option.

Option 2: natural person authorizes a professional broker to manage its investment portfolio

Income from individual management of financial instruments is formed as positive difference between the value of all assets that natural person has transferred to the manager of portfolios during the management contract term and the value of all assets that the natural person has withdrawn from investment portfolio (Section 119 Paragraph 11 Clause 5 of the PIT Law). Earned income has to be declared in annual income declaration.

In the situation mentioned in the example, in 2018, financial assets were not withdrawn from the financial instruments account, therefore, there are no not PIT taxable income Accordingly no obligation to submit declaration and pay PIT.

Natural person received taxable income on 5 June 2019 when natural person withdrew more assets from the financial instruments account than invested. Therefore, natural person, until 1 June 2020, has to submit annual income declaration where the received income has to be declared and pay to the state budget PIT of EUR 1,291 ((EUR 81,453 – EUR 75,000) * 20%).

Compared to Option 1, the procedure of determining and declaring income is simpler in Option 2, as every financial transaction does not have to be declared but the asset flow in the financial instruments account has to be tracked (i.e., in-coming and out-going payments from the account), and in case of this option, tax liabilities do not occur while more money is withdrawn from the account than it is invested. However, PIT liabilities in Option 2 are higher than in Option 1, as in Option 2, PIT taxable income cannot be reduced by non-taxable income, i.e., Latvia state bonds, and by the income, from which the income payer has already withheld income tax at the moment of payment of income. Income from dividends which is exempt from PIT according with Section 9 (1) 2.1) of the PIT Law also has the same negative impact on the PIT liabilities as this type of income cannot be excluded from the amount of taxable income.

Therefore, if it is planned to perform transactions with financial instruments that are exempt from PIT (listed in Section 9 (1) of the PIT Law) or from which PIT is withheld by the income payer, Option 2 is not recommended from the point of view of PIT.

If Option 3 would not exist, Option 2 would be recommended for those who plan to operate in long-term and actively in the financial market, as this option entitles person to sum up income earned from transactions with financial instruments for several years. However, as there is Option 3, it is recommended to assess it, as it is, in its essence, improved Option 2.

Option 3: financial instruments account with special mark or reference to the status of investment account for the purposes of PIT Law

The same as in Option 2, in Option 3, PIT taxable income occurs when the amount of assets withdrawn from the investments account exceeds the amount of assets paid in the investment account. While assets (i.e., money or securities) are not withdrawn from the account in the amount that exceeds the invested amount, PIT liabilities do not occur. In Option 3, compared to Option 2, several advantages exist. Namely, PIT taxable income can be reduced by the income that is exempt from PIT (for example, income from Latvia state bonds) and by income from which PIT has been already withheld by the income payer. If PIT has been withheld partially, PIT taxable income is reduced in proportion to income from which tax has been withheld according to the rate determined in the Section 15, Paragraph five of the PIT Law. Other positive aspects of Option 3 include the opportunity to transfer financial instruments between investment accounts based on their acquisition value, thereby not causing PIT liabilities from financial instrument that is transferred between investment accounts.

However, when investment account is opened, restrictions and conditions prescribed in Section 1113 of the PIT Law have to be considered in regard to transactions with assets in the investment account (for example, securities cannot serve as security in purchase of immovable property) to ensure that financial instruments account would not lose the status of investment account prescribed in the PIT Law. Restrictions in regard to provider of investment services shall be considered, too.

In the example, natural person does not have PIT liabilities in 2018, as assets were not withdrawn from the financial instruments account.

Natural person had PIT taxable income in 2019 only, when natural person withdrew more assets from the financial instruments account than invested. Natural person has to declare earned income of EUR 3,333 (i.e., (EUR 81,453 – EUR 75,000 – EUR 2,000 – EUR 220 – EUR 300 – EUR 1,000/2 – EUR 100) * 20%)) in the annual income declaration for 2019 until 1 June 2020 and PIT of EUR 667 has to be paid to the state budget.

Compared to Option 1 and Option 2, in Option 3, natural person has the lowest PIT liabilities. Although determining taxable income might seem the simplest, it is not the case, as calculation of taxable income requires deduction of income that is exempt from PIT and from which tax has been withheld already. However, it should be noted that some credit institutions offer their customers investment account report that eases the process of determining the amount of taxable income and the moment of declaration.

Although, in the example we concluded that Option 3 is the most favourable, it should be noted that situations differ and, depending on types of transactions and your goals, it can have different impact on PIT liabilities.

Information prepared by Leinonen Latvia, Tax & Legal Advisory Department.